Bank loans obtained by the candidate

If a candidate obtains a bank loan or a loan derived from an advance on the candidate’s brokerage account, credit card, home equity line of credit or other line of credit, and the loan is used for campaign-related purposes, the committee must report the loan from the candidate as a receipt. Both the original loan and payments to reduce principal must be reported on Schedule C for each reporting period until the loan is repaid. A committee that obtains a loan from a bank must also file Schedule C-1 with the first report due after incurring the new loan. Loans obtained by an individual prior to becoming a candidate that are subsequently used to influence the candidate’s election to Federal office must be reported as an outstanding loan owed to the candidate by the principal campaign committee, if the loan is outstanding at the time an individual becomes a candidate.

Reporting on candidate forms

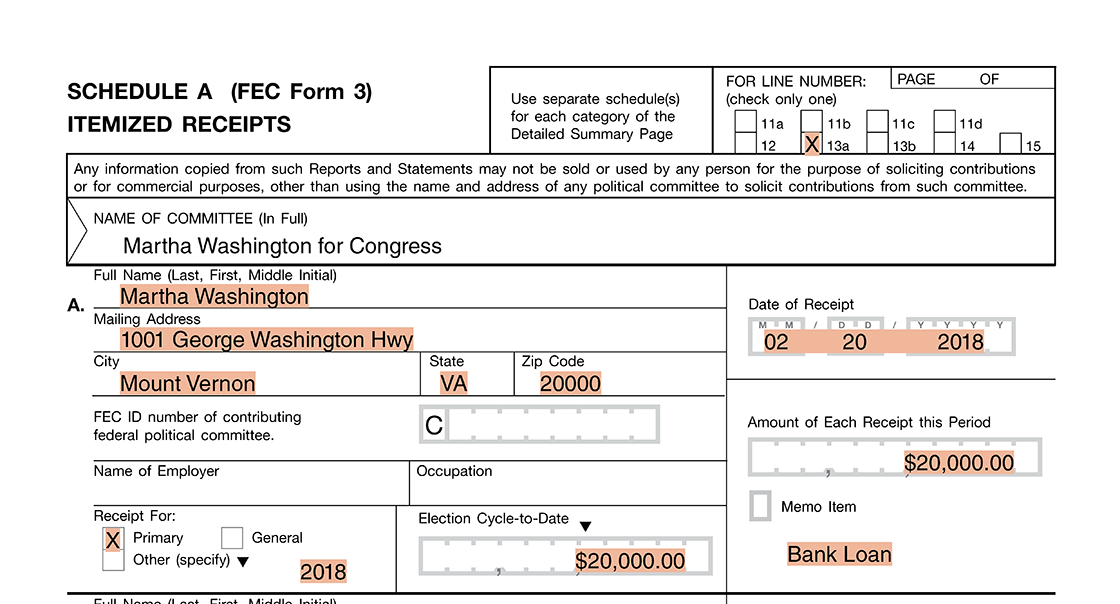

House and Senate committees report bank loans or loans derived from advances on the candidate’s brokerage account, credit card, home equity line of credit or other line of credit obtained by the candidate on Form 3, Line 13(a). The committee itemizes receiving the loan, regardless of the amount, on Schedule A, supporting Line 13(a).

For example, Martha Washington obtains a $20,000 loan from the bank and loans the money to her principal campaign committee.

The committee reports receiving Martha Washington’s loan for $20,000. The entry on Line 13(a) itemizes the candidate’s information, the loan amount, the date the loan was made, and the loan’s election designation of Primary 2018. The source of the loan is clearly noted as “bank loan.”

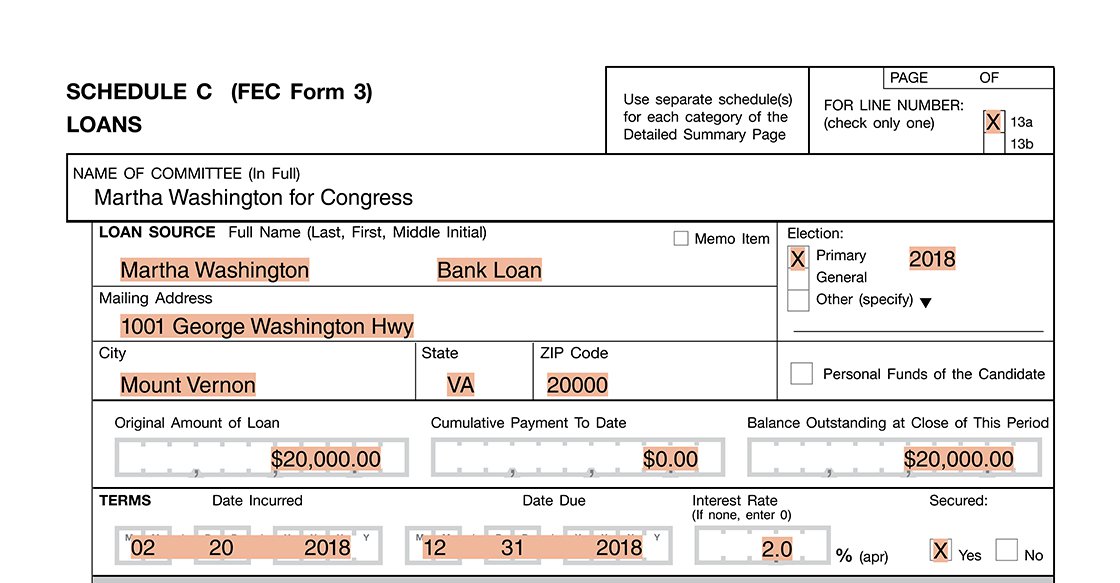

When the committee discloses receiving the loan, it will also disclose details about the loan, including the type of loan the candidate receives (i.e., bank loan, brokerage account, credit card, home equity line of credit, other line of credit, personal funds of the candidate) on Schedule C. Schedule C will be filed continuously for each reporting period until the loan is paid off. It will show the loan’s original amount, the terms between the candidate and the committee, payments made, and the outstanding balance at the close of the reporting period.

Schedule C shows details about the loan, including the loan terms between the candidate and the committee. The date the loan was incurred is disclosed along with a due date and interest rate. Candidates can decide to charge committees less than market interest rates and not set a due date. Be sure to disclose “none” or something similar instead of leaving the due date or interest rate fields blank. The committee noted “bank loan” so that the source of the loan is clear on the report.

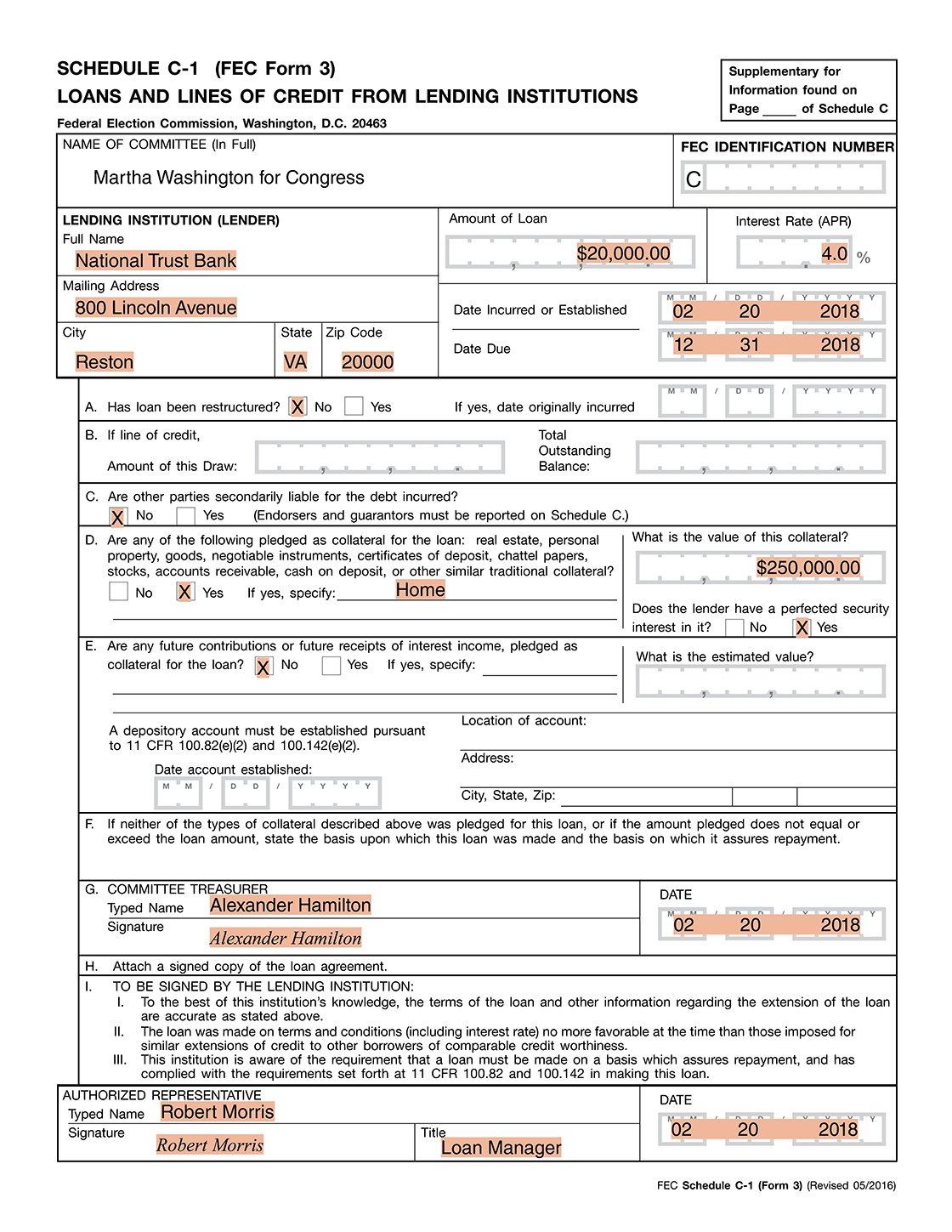

The committee must also file a Schedule C-1 to disclose the terms between the candidate and the bank or other permissible lending institution with the first report due after a new loan or line of credit has been established. A new Schedule C-1 must also be filed with the next report if the terms of the loan or line of credit are restructured. Additionally, in the case of a candidate that has obtained a line of credit, a new Schedule C-1 must be filed with the next report whenever the candidate draws on the line of credit. For loans derived from a candidate loan, the reporting on Schedule C-1 is simplified. For electronic filers, the Schedule C-1 can be filed electronically. For this type of loan, neither the treasurer’s signature nor lender certification is required. The committee is not required to submit the loan agreement to the Commission.

Schedule C-1 shows details about the loan, this time listing loan terms between the candidate and the bank. This means the loan's due date and interest rate reported on Schedule C-1 may differ from what is reported on Schedule C. In this case, the bank is charging the candidate 4.0% interest, but the candidate is only charging the committee 2.0% interest. The Schedule C-1 also shows the collateral that the candidate is using to secure the loan.

Learn more about reporting other forms of candidate support:

Reporting with FECFile

Enter the loan in the Loans, Debts and Obligations tab. Click the “Schedule C-1” button to enter information about the loan and the terms between the candidate and the bank.