In-kind contributions with appreciated value

When a committee receives an in-kind contribution whose value may appreciate over time, such as stock or artwork, special reporting rules apply.

Reporting on candidate forms

House and Senate committees report appreciated goods on Form 3. The line number used to report receiving the in-kind contribution depends on who is giving the in-kind contribution.

Itemize the initial gift as a memo entry on Schedule A if it:

exceeds $200 or

aggregates over $200 when added to other contributions received from the same source during the election cycle.

In the “Amount” field, report the fair market value of the contribution on the date the item was received. Do not include that amount in the total for the appropriate contribution line 11(a), 11(b), 11(c) or 11(d) on the Detailed Summary Page. No itemization on Schedule B is necessary.

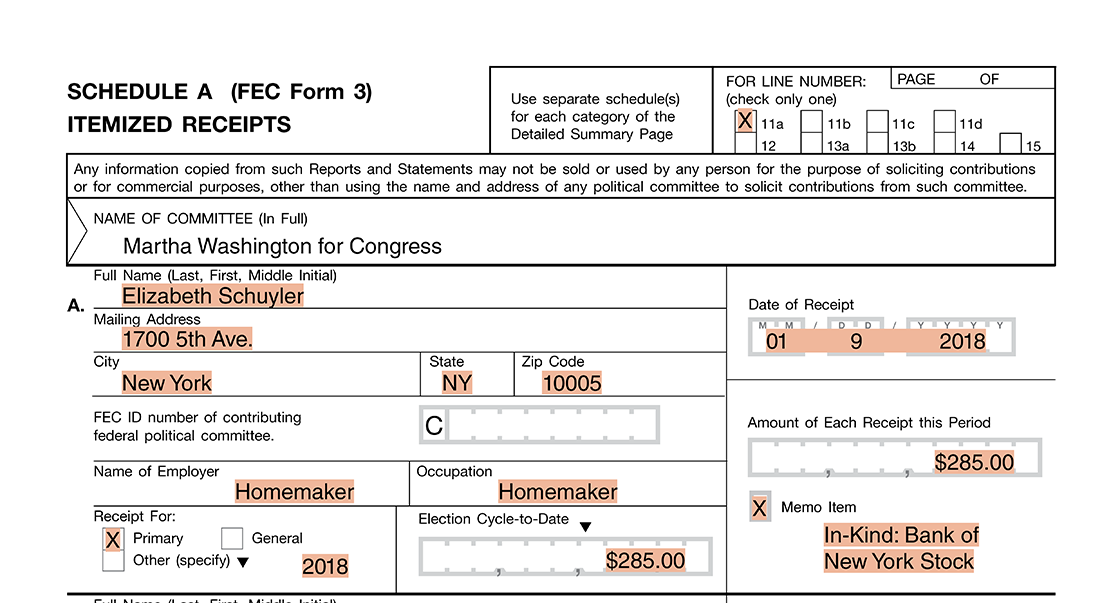

The committee received stock from Elizabeth Schuyler worth $285. Since the contribution is from an individual, the stock is reported on Line 11(a)(i). The committee gives Elizabeth's mailing address, employer and occupation information, as well as the date and amount of receipt, election designation, and aggregate election cycle-to-date total for the contributor. The committee includes a notation that they received an “In-kind: Bank of New York Stock.”

Once the item is sold, report the sale price as a contribution on the appropriate line (such as 11(a) for a contribution from an individual) if the purchaser is known or as an “other receipt” on Line 15 if the purchaser is unknown. Itemize the transaction on Schedule A if it meets the itemization criteria above. If the purchaser is known, the amount of the purchase, when aggregated with other contributions by the purchaser, must fall within the contribution limits.

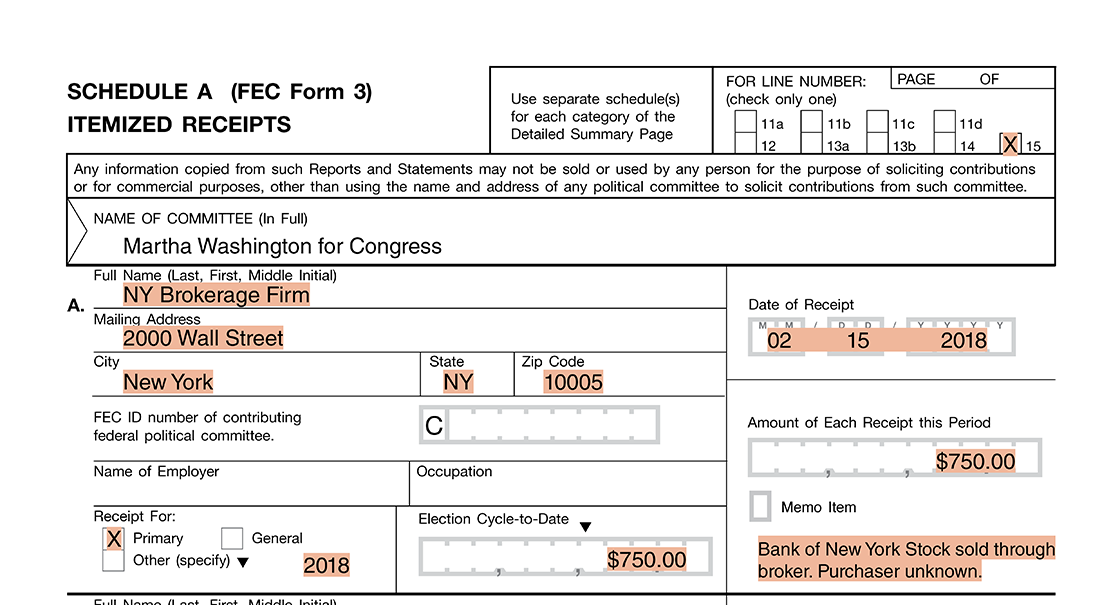

The committee sells the stock through a broker for $750. Since the committee doesn’t know who bought the stock, the committee reports the brokerage firm, its address information, the date and amount of receipt, and the aggregate election cycle-to-date total on Line 15, “Other Receipts.” The committee included the notation “Bank of New York stock sold through broker. Purchaser unknown.”

Reporting with FECFile

To enter receiving the in-kind good that will appreciate, go to the Summary Page tab, right click on the contributor’s category and select “new.” Enter the contributor’s information and check the “memo” box. Include a note about the type of in-kind that is received.

To enter the sale of the in-kind, go to the Summary Page tab, right click on the contributor’s category and select “new.” Enter the contributor’s information. Add a description of the in-kind that was sold and whether or not the purchaser was known to the committee.